As of today, most of the economies of the world, including the American economy, are defined by compounding investment returns.

At one end of the scale, much of the U.S. retirement system currently relies on individual 401(k) accounts. Workers make many investments and reinvestments over the course of their employment. More specifically, with the goal of finally cashing out when they retire.

What are Compounding Investment Returns?

Compounding Investment returns is the ability of an asset to create earnings, which are then reinvested or remain invested with the objective of creating their own earnings, that is referred to as compounding.

To put it another way, compounding refers to the process of creating earnings from past earnings.

Compound returns are when the value of your investment rises as a result of both the initial capital and the returns created by that investment. It is another way of describing investment returns.

How Does Compounding Investment and Returns Work?

To understand how compounding investment and returns work, consider the following scenario:

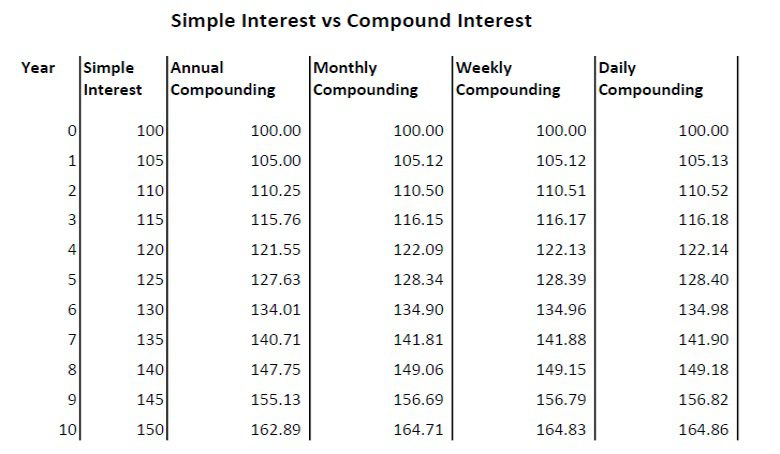

You make a $1,000 investment that returns a 10 percent yearly compound rate of interest. At the end of the first year, you would have $1,100. It included the original money you invested plus a $100 return on your investment, representing a 10 percent return.

The amount you would have at the conclusion of the second year is $1,210.

You would have $1,331 at the end of the third year, $1,464 at the end of the fourth year, and $1,610 at the end of the fifth year if you kept going.

Because the interest rate compounded annually, your account increased in value by more than $100 per year.

It applied to the account’s whole value, which included both the capital and any profits or losses.

As a result, you received 10 percent of $1,000 in your second year, 10 percent of $1,210 in your third year, and so on.

Generally speaking, the mechanics of compound returns are rather straightforward.

When you make an ordinary income-generating investment, the holder of that investment gives you a check when the investment creates money for him or her.

For example, when a bond pays interest, the bond company may send you a check for the amount equal to the interest rate paid.

Compound Investment and Income

A compound return investment produces income as well as capital gains.

However, in contrast to a traditional product, the holder of the investment retains the income generated by the investment.

Moreover, adds it to the principal invested by you.

Afterward, when it is time to compute your return on that investment, the new value of your account is used as a foundation for the computation.

This procedure repeats each time the asset earns a return on its investment.

Consequently, if you are paid quarterly, the company reinvests your money and recalculates it four times each year; if you are paid yearly, the company does it once per year; and so on.

What Is the Value of Compound Investment Returns?

Compound returns are one of the most lucrative investment forms available. As well as one of the most expensive types of debt available in the whole field of finance.

The importance of compound interest is so widely recognized that an apocryphal quotation is ascribed. Einstein describes it as “the most powerful force in the universe.”

Take, for example, our previous example.

We have deposited $1,000 into a checking account that earns 10% annual interest.

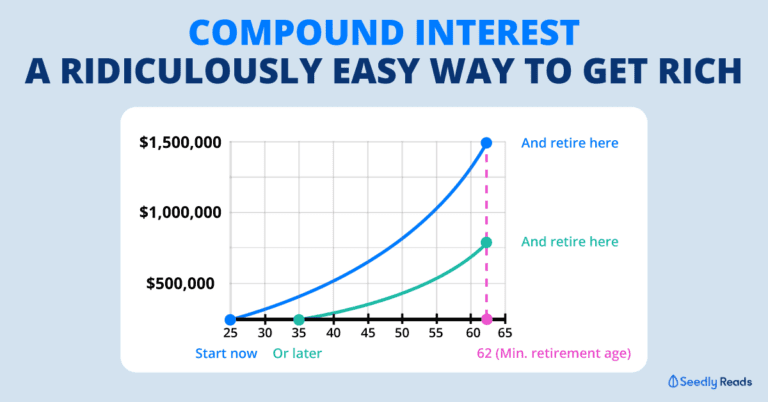

Let’s pretend it’s part of a retirement plan, and we leave it alone for the next 40 years.

When we retire at 65, the money we put down in our mid-20s will have grown to more than $45,000, thanks to compound interest.

In addition, our case is a little improbable.

It is substantially more probable that this investment would multiply quarterly.

Resulting in a total value that is slightly shy of $52,000.

A single impulsive investment made when we were 25 years old can now supply us with a whole year’s income.

Especially, in our golden years.

That is the power of compounding.

Compound returns may provide you with some of the greatest investments available in the market if you are investing for the long term.

In the near run, they are frequently not extremely valuable assets.

Compound return investments, on the other hand, will seldom deliver the type of speculative returns that, for example, a rocket stock may bring.

However, compound investments have the potential to generate considerable growth over time since the value of the investment grows by adding (literally compounding) upon itself.

How Do Investment Products offer Compound Returns?

In order to generate compound returns, an asset must fulfill a few fundamental requirements:

Dividends, interest, or some other kind of income stream must be paid to the asset’s owner in order for the asset to be considered a successful investment.

It cannot be an asset whose worth is only appreciated when the asset is sold or otherwise transferred.

Those returns must be reinvested back into the underlying principle that was utilized to compute your gains by the investing company.

The use of financial products can do this in a variety of ways.

Interest Payments

This is the example that we’ve used throughout this post to illustrate our point.

The investment will generate a fixed rate of return computed on the basis of the underlying principle, and any profits will add to this underlying principle in order to raise the rate of return.

Asset Holdings

In this case, the investment is based on a collection of assets, such as a stock portfolio, and it derives its value from any income provided by the assets in the collection.

All profits reinvested in the acquisition of more assets, therefore expanding the number of holdings that are capable of generating income on a continuing basis.

Which Investment Products Provide Compound Returns?

Compound returns are available through a variety of investment options. Some of the most often encountered are as follows:

Mutual Funds

A large number of Mutual Funds offer compound interest.

The most typical structure, in this case, is for the fund to invest in equities that pay dividends to investors.

It then utilizes those dividends to purchase further shares of stock.

Resulting in you receiving even more dividends during the following cycle (since you hold more shares).

Exchange Traded Funds (ETFs)

ETFs with compound returns are also widely available.

They function in a similar way to mutual funds in that they generally invest in dividend-paying equities.

In exchange for your dividends, the fund purchases additional shares of stock on your behalf. Rather than issuing you a cash check.

Your dividend check grows in size the next time the stock pays its owners.

Moreover, the ETF reinvests the extra money into your account.

Certificates of Deposit

A certificate of deposit (CD) is a type of investment product that banks issue you.

CDs with compound interest are certificates of deposit that pay a fixed rate of interest that compound on regular basis.

Moreover, they have a specified maturity date.

It functions in the same way as our previous example.

Every time an interest payment incurs on a CD, the bank immediately adds that payment to the underlying principle.

When the CD matures, you get the whole amount you invest.

Zero-Coupon Bonds

A zero-coupon bond is a type of bond that pays compound interest, with the rate of interest, the repayment schedule, and the date of repayment all predetermined in advance.

The face value of the bond represents the amount of money it will be worth when it matures. When you acquire a bond, you pay the bond’s face value today.

It is equal to what the bond’s face value is worth.

How Can Investors Receive Compounding Returns?

Simply defined, compound interest is beneficial to investors, although the term “investors” can refer to a wide range of people.

In the case of financial institutions, compound interest is beneficial when they lend money and then reinvest the interest they get in the form of further loans.

Those who have bank accounts, bonds, or other assets will also profit from compound interest. Since they will earn interest on their money over time.

In addition, while the term “compound interest” incorporates the word “interest”.

It is crucial to highlight that the idea extends beyond instances in which the word “interest” commonly employed. More likely, bank accounts and loans.

Compounding Investment Returns – Final Verdict

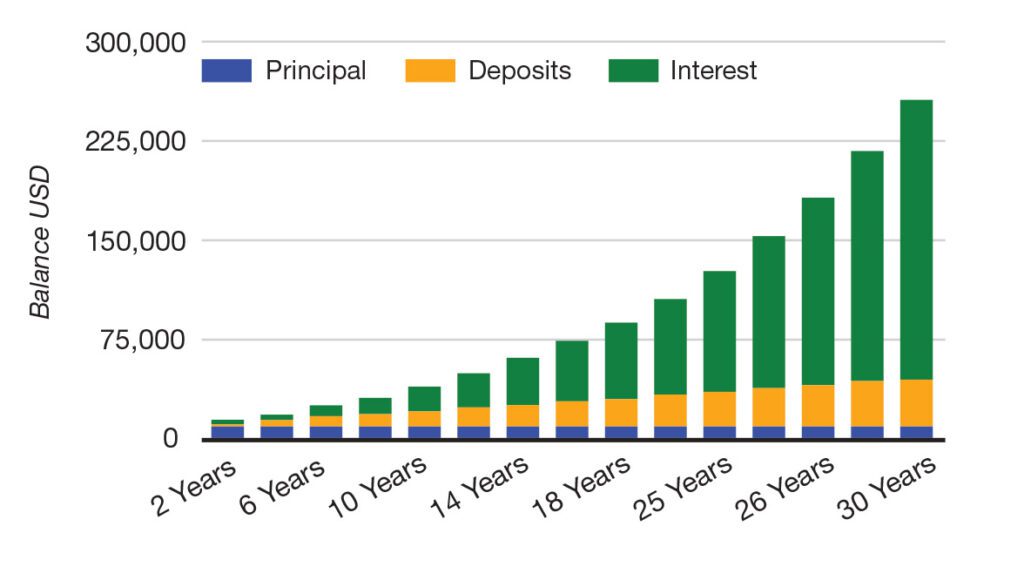

Probably the most exciting part of the power of compounding is that your investments generate interest.

On both the initial money and the interest that you already earned on your investments.

Overall, the force of compounding allows you to develop a large foundation of profits that add to every cycle, allowing you to make more money.

To be a successful investor, you must understand that the strength of compounding comes in its capacity to reinvest the profits made on your initial investment.

In other words, you should avoid attempting to take your profits at any point throughout the investing term prior to the end of the period.

Alternatively, you would run the danger of restricting the growth potential of your profits. It is due to the power of compounding on your investments.

The investment plan and time period that you choose should reflect your financial objectives. As well as your capacity to invest.

The greater the distance between you and your objective, the sooner you must begin investing. In order to have enough time to build the necessary quantity of cash.

Hold a Master Degree in Electrical engineering from Texas A&M University.

African born – French Raised and US matured who speak 5 languages.

Active Stock Options Trader and Coach since 2014.

Most Swing Trade weekly Options and Specialize in 10-Baggers !

YouTube Channel: https://www.youtube.com/c/SuccessfulTradings

Other Website: https://237answersblog.com/